Table of Content

Investopedia requires writers to use primary sources to support their work. These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in oureditorial policy. Make a change that will unequivocally benefit the consumer throughout the remainder of the plan. D. The consumer permits the filing of a lien senior to that held by the creditor.

“If approved, this will result in a single, regular monthly payment, although you will lose the ability to make future draws.” If you choose this route, research closing costs and current mortgage rates. Most lenders notify customers at least six months before the end of their draw period. However, if you’re unsure of when the loan will move into repayment, contact your lender’s service department. The draw period of a HELOC works like an open line of credit.

options to pay off your HELOC

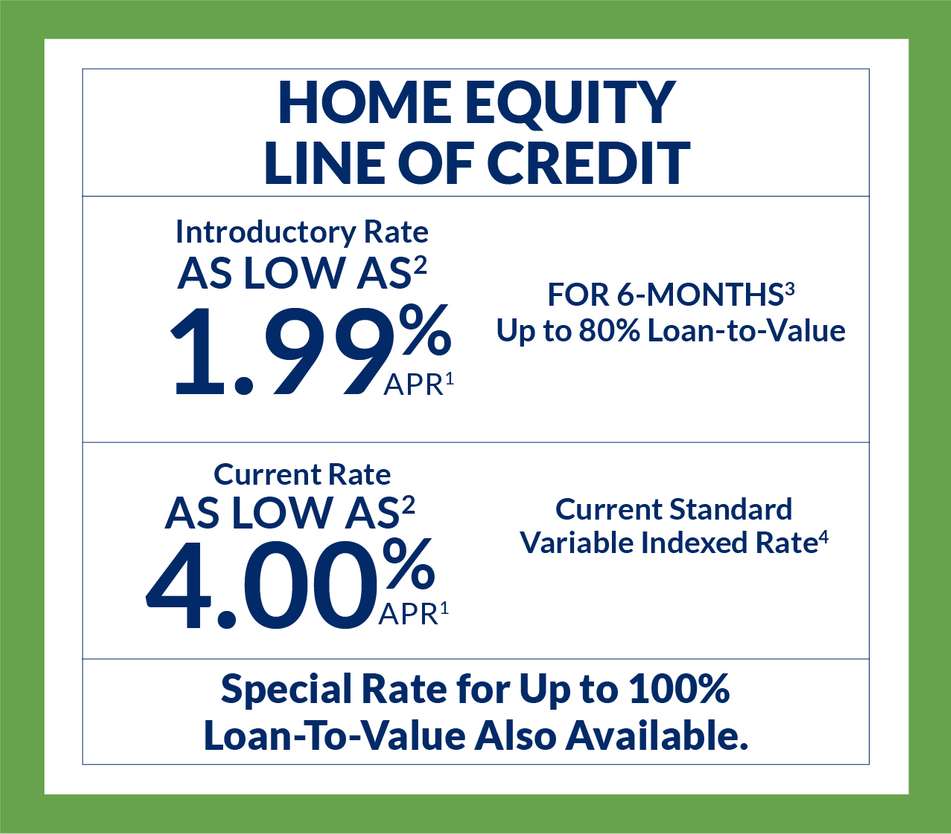

In most cases, HELOCs have variable interest rates. However, there may be an opportunity to transfer it to a fixed interest rate. “Most banks will have a fixed-rate option for repayment as part of the HELOC, but you may need to set that up prior to the end of the draw period,” says Giles. “Contact your bank and ask,” he recommends. During the draw period, you were only required to make payments against the interest. Once you enter into the HELOC repayment period, you’ll have to make full amortized payments, meaning you’ll pay against the principal and interest.

At Bankrate we strive to help you make smarter financial decisions. While we adhere to stricteditorial integrity, this post may contain references to products from our partners. Here's an explanation for how we make money. Matthew Goldberg is a consumer banking reporter at Bankrate.

Alternative Repayment Options

Your draw period is typically a set number of years, often 10 years. When taking out a home equity line of credit , the HELOC draw period is your chance to spend the money you borrow before you have to pay it back. It’s the first step once you’ve closed on your HELOC, a flexible way to borrow against the equity you’ve built up in your property.

Don’t count on being able to refinance out of a balloon payment. Also make sure that you know the terms of any HELOC before signing up for one. Be aware of the length of your draw and repayment periods and make sure that there are no prepayment penalties if you choose to make additional payments toward your principal during your draw period.

When to Refinance your Mortgage

Disclosure of annual percentage rate - more conspicuous requirement. As provided in § 1026.5, when the term annual percentage rate is required to be disclosed with a number, it must be more conspicuous than other required disclosures. Once you access the line, you begin to pay interest on the amount you've used. The interest rate is floating, meaning it can change daily.

We do not cover every offer on the market. Editorial content from NextAdvisor is separate from TIME editorial content and is created by a different team of writers and editors. Take control of your financial future with information and inspiration on starting a business or side hustle, earning passive income, and investing for independence.

HELOC Draw Period

The disclosures could be located on the same Web page as the application without necessarily appearing on the initial screen, immediately preceding the button that the consumer will click to submit the application. When inquiring about a mortgage on this site, this is not a mortgage application. Upon the completion of your inquiry, we will work hard to match you with a lender who may assist you with a mortgage application and provide mortgage product eligibility requirements for your individual situation.

Our Learning Center provides easy-to-use mortgage calculators, educational articles and more. And from applying for a loan to managing your mortgage, Chase MyHome has everything you need. You will have access to your new HELOC’s available credit as long as the balance you are refinancing doesn’t exceed your credit line limit. Since you will be opening a new HELOC with Chase to pay off the balance of your current account, you can think of the refinancing process as a re-application. You may also choose to do this on your own through a lump-sum payoff option, or by getting ahead on your HELOC payments.

“Plan accordingly and don’t get caught off guard by the larger payment amount,” said Eric Aved, senior vice president and home equity product executive at Bank of America. A home equity loan is a consumer loan allowing homeowners to borrow against the equity in their home. The interest paid on a home equity line of credit used to be tax deductible, but the law changed with the Tax Cuts and Jobs Act of 2017. Now HELOC interest can only be deducted on the amount of the HELOC used to “buy, build, or substantially improve” a home. Doretha Clemons, Ph.D., MBA, PMP, has been a corporate IT executive and professor for 34 years. She is an adjunct professor at Connecticut State Colleges & Universities, Maryville University, and Indiana Wesleyan University.

This insurance was used by lenders to “securitize pooled mortgages through the National Housing Act Mortgage-Backed Securities program”. Another measure was the Office of the Superintendent of Financial Institutions decision to cap the maximum LTV ratio for HELOCs at 65%, thus limiting the amounts homeowners could leverage from their property. Underwriting rules were also made stricter through the Residential Mortgage Underwriting Practices and Procedures Guideline. HELOC abuse is often cited as one cause of the subprime mortgage crisis in the United States.

For example, creditors may not include “boilerplate” language in the agreement stating that they reserve the right to change the fees imposed under the plan. In addition, a creditor may not include any “triggering events” or responses that the regulation expressly addresses in a manner different from that provided in the regulation. Similarly a contract cannot contain a provision allowing the creditor to freeze a line due to an insignificant decline in property value since the regulation allows that response only for a significant decline. The HELOC end of draw period is when you enter the repayment phase of your line of credit. You are now required to begin paying back the principal balance in addition to paying interest.

Thus, for example, if negative amortization cannot occur in a home equity plan, a reference to it need not be made. When we say that the jump is drastic, we are not exaggerating. In this example, we are assuming a 20-year repayment period and only a 3% interest rate. Knowing the full amount of the principal and interest payment before you enter the repayment phase helps you avoid surprises. Principal and interest payments can cause a significant change to a budget, and these payments will last anywhere from 10 to 20 years. However, if your HELOC balance is already at zero at the end of the draw period, your account will typically close automatically.

What to know before your draw period ends

HELOCs are typically variable-rate loans, meaning the interest rate you pay is based on the market and reset every so often. During the draw period, you typically have to make minimum payments on the loan, which can often be interest-only. At the end of the draw period, you may be able to renew your line of credit and restart the clock. Otherwise, you’ll enter the repayment period of the loan. A creditor may change the annual percentage rate for a plan only if the change is based on an index outside the creditor's control.

The one exception is that if the replacement index is the spread-adjusted index based on SOFR recommended by the Alternative Reference Rates Committee for consumer products to replace the 1-month, 3-month, 6-month, or 1-year U.S. For fixed-rate plans, a recent annual percentage rate is a rate that has been in effect under the plan within the twelve months preceding the date the disclosures are provided to the consumer. If an event permitting termination and acceleration occurs, a creditor may instead take actions short of terminating and accelerating. For example, a creditor could temporarily or permanently suspend further advances, reduce the credit limit, change the payment terms, or require the consumer to pay a fee. A creditor also may provide in its agreement that a higher rate or higher fees will apply in circumstances under which it would otherwise be permitted to terminate the plan and accelerate the balance.

No comments:

Post a Comment